Are hospitalists going to get a Medicaid pay raise for 2013 and 2014? The answer is yes, hospitalists qualify for Medicaid parity (with Medicare) as required by the Affordable Care Act (ACA). For many states, Medicaid pays physicians and other providers

a fraction of Medicare rates. Legislation signed as part of the ACA mandates Medicaid rates to equal 100% of Part B Medicare rates in calendar year (CY) 2013 and 2014. That means if you haven't already seen increased rates, and you are a qualified physician providing qualfied primary care services, you will get increased Medicaid payments retroactively applied to January 1st, 2013.

When folks think of primary care, most likely think of the outpatient clinics for pediatrics, family medicine and internal medicine physicians. But that's not how ObamaCare defines a primary care specialty. That's right people, hospitalists, pediatric cardiologists and a whole lot of other practicing physicians now qualify as providers of primary care under ACA rules.

I was first alerted to this stunning CY 2013 and 2014 increase in Medicaid payments for hospitalists after reading an article from

The Hospitalist titled

Afordable Care Act (ACA) Provision Carries Pay Raise For Some Hospitalists. Joshua Bowell, the Society of Hospital Medicine's senior manager of government relations, discusses the rules and how they apply to hospitalists. It's a great article and I encourage all hospitalists to click the link above, read it and forward it to their billing company to make sure all necessary paperwork has been filed to qualify for increased Medicaid payments and retroactive Medicaid payment increases that are required to start on January 1st, 2013.

What are the specifics of this law? You can read the Fall 2011 rule abstract that implements section 1202 of the Affordable Care Act (ACA)

here. I have taken the liberty of publishing it below for your review:

Title: Payments for Primary Care Services Under the Medicaid Program (CMS-2370-P)

Abstract: This proposed rule would implement section 1202 of the Affordable Care Act that requires payment by State Medicaid agencies of at least the Medicare rates in effect in calendar years (CYs) 2013 and 2014 for primary care services delivered by a physician with a specialty designation of family medicine, general internal medicine, or pediatric medicine. This rule would implement the statutory payment provisions uniformly across all States. Specifically, this proposed rule would define, for purposes of enhanced Federal match, eligible primary care providers and identify eligible primary care services, as well as specify how the enhanced payment should be calculated. This proposed rule would also provide general guidelines for implementing the enhanced payment for managed care services.

So how does a hospitalist and a pediatric cardiologist qualify for primary care under the proposed rule above? Great question. To understand the answer, one must understand how the rule defines the qualified physician providing the qualified primary care service. I did a little digging to find out how. Do you know how hard it is to find all this stuff? The

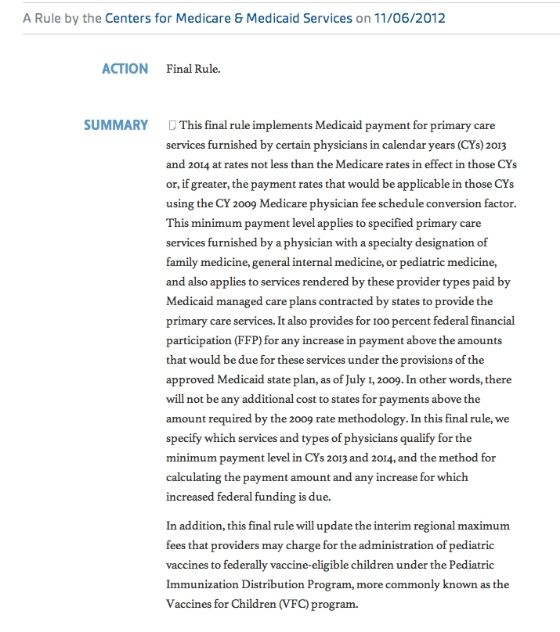

November 6, 2012 Federal Registrar published the final ruling (with a

minor correction published December 14th, 2012) titled RIN 0938-AQ63 as it applies to the regulation mandating Medicaid parity with Medicare Part B payments for qualified primary care physicians. Here is the lead summary paragraph of the final ruling:

How does this final ruling define a physician delivering a primary care service? According to the Federal Registrar, the November 6th, 2012 final ruling amends several sections of the Social Security Act, specifically, 1902(a)(13), 1902(jj), 1932(f), and 1905(dd). Effective March 20th, 2010, section

1902(jj) of the Social Security Act now defines a primary care service as follows:

There you have it folks. ObamaCare has defined, through amendment of the Social Security Act, exactly what primary care services are. It is the delivery of

evaluation and management services to title XVIII beneficiaries. Title XVIII is Medicare. It appears to me that any physician that submits payment for a qualified E&M charge is submitting a service for a primary care service. What are the

E&M codes eligible to receive higher Medicaid payments? Evaluation and Management codes 99201-99499 of the Healthcare Common Procedure Coding System (HCPCS) and vaccine administration codes 90460, 90461, 90471, 90472, 90473 and 90474 have been lawfully determined to qualify for Medicaid parity payments in CY 2013 and 2014.

As a hospitalist, that means most E&M charges qualify for higher Medicaid payments. All initial hospital codes, subsequent care codes, critical care codes, observation codes, and same day admit/discharge codes are included by law. Yes folks, my critical care is considered primary care. And my emergency room codes? If I see a patient in the emergency room and decide not to admit them, my emergency department E&M code is considered a primary care service. Sorry ER doctor, even though you submit the same code, you do not get parity under this law. But why? For many ER doctors, they are the Medicaid patient's primary care provider through dozens of ER visits a year. If any doctor is the primary care doctor for a Medicaid patient, it's the ER physician because no primary care doctor will see them! Why can't they get paid the higher rate?

Does any physician who submits an E/M code get parity payments for their primary care service? Can a urologist get paid Medicaid parity for their office visits? Can a general surgeon get Medicaid parity for their cholecystectomy? The answer is no. Why can a pediatric cardiologist get Medicaid parity but a general surgeon can not? The answer lies in how ObamaCare defines an eligible physician. Return back to the summary statement above and you'll see the physician must have a specialty designation of family medicine, pediatric medicine or general internal medicine. A urologist and general surgeon does not meet that requirement. But how does a pediatric cardiologist make the cut?

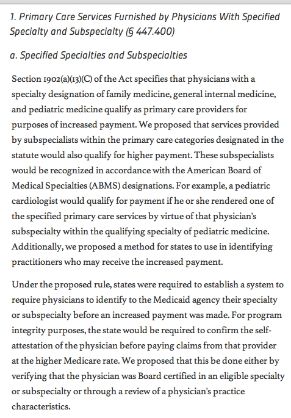

The answer lies in this law's interpretation. After the proposed rule was published in May, 2012, one hundred and seventy-seven comments were received. Some of those comments reviewed below helped clarify the who is an eligible physician question. Read this section thoroughly to fully understand who qualifies and who doesn't. Click on the picture to take you directly to the Federal Registrar paragraph contained within.

And that folks is how a pediatric cardiologist gets a Medicaid pay increase for their E&M services in CY 2013 and 2014. The interpretation of this law adds

44 additional specialty designations to the qualifying list for Medicaid parity. What is the gist of the argument? A pediatric cardiologist is trained in the specialty designation of pediatric medicine and thus qualifies for Medicaid fee increases to match Medicare payment rates for 2013 and 2014. The law says if a physician is recognized by the American Board of Physician Specialities (ABPS), the American Board of Medical Specialties (ABMS) or the American Osteopathic Association (AOA) as a specialist or subspecialist within the primary care categories, they receive Medicaid parity for their E/M charges.

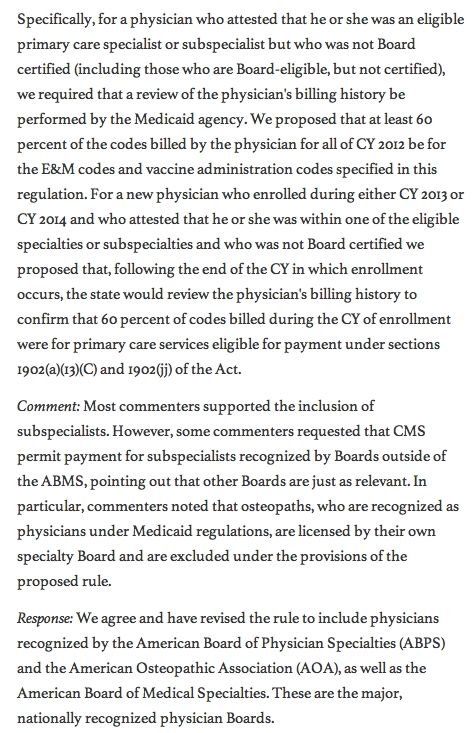

What if the physician is not certified by any of these boards? The law allows for Medicaid pay raises if 60% of the codes billed in the calendar year of enrollment were for qualified primary care services that has been defined above. I suspect the 60% applies to the absolute number of codes submitted and not 60% of the total RVU value for the calendar year. If the answer is absolute codes, then almost any qualifying physician could qualify by virtue of submitting at least two E&M codes for every non E&M procedure code done in the procedure suite. That would give them a 66% rate of E&M charges which is above the required 60% threshold. I'm confident most medical subspecialists could clear the 60% threshold with no problem as long as they average at least two E&M charges for every non E&M procedure code they provide on any given day.

What about services provide by nonphysician practitioners? Do nurse practitioners, pharmacists, midwives, certified registered nurse anesthetists or other qualified nonphysician practitioners receive the mandatory increases in Medicaid payments? The answer is only if they are billing under the supervision of an eligible physician. That means the answer is

no for independent nonphysician practitioners but

yes if they are working with physicians in the qualified specialties listed above. Seems silly, doesn't it? A pediatric cardiologist can spend 80% of their time in the cath lab doing procedures, but if they submit at least 60% of their codes as E&M charges they can get Medicaid parity on their office visits, hospital consults and hospital follow-up codes. But the independently practicing certified nurse midwife administering the flu shot to protect mom and baby cannot.

Oh, and sorry OB/Gyn doctors. You may be the only physician for your patients and provide 100% primary care to 80% of your patient population, but you don't qualify for federal subsidized Medicaid fee increases because you didn't train in pediatric medicine, family medicine or general internal medicine. Maybe you should have been a pediatric cardiologist instead. ObamaCare says they are providing massive amounts of primary care these days, and by primary care, I mean telling the patient to contact their primary care provider to fill out the Family Medical Leave Act paperwork so they can have mom and dad at the bedside while they take Junior to the cath lab.

What about states that don't plan on expanding Medicaid eligibility? That has no bearing on the requirement for eligible physicians providing eligible E&M services to get paid 100% of their Part B Medicare rate on their Medicaid charges for CY 2013 and 2014. Whether states decide to expand Medicaid or not, qualified doctors providing qualified E&M charges get a raise on their Medicaid payment rates.

What happens after 2014? As noted in the Federal Registrar, states are required to report Medicaid participation rates to Congress in anticipation of decisions to continue or discontinue the current federal subsidy for qualifying Medicaid charges. I'm sure that's going to be another political fight. I've asked a few of my colleagues about what they intend to do with Medicaid. All of them say they have no intention of expanding their clinic slots to include a greater proportion of Medicaid patients. My

facebook post confirms that. They can easily fill up their clinic with follow-up visits on their current panel of patients with chronic disease. I suspect after these two years are up we're going to see no increase in Medicaid participation. Physicians don't run their business on a two year horizon. Imagine expanding a clinic to include a large influx of Medicaid patients only to try and balance the budget based on unstable Medicare politics and a Medicaid policy that falls off the cliff after CY 2014.

What physician in their right mind would budget that? I'm willing to bet almost none. The quirks of this law are simply mind boggling. Pediatric cardiologists and hospitalists will get Medicaid parity for their ICU work but an independently practicing certified nurse midwife trying to take care of mom and baby as the only provider from conception to birth will not. I don't need to say anything more. Oh yeah, one last thing. How much is this little experiment going to cost? The expected cost to the federal government for this Medicaid parity pay increase is 5.6 billion dollars in calendar year 2013 and 5.745 billion dollars in 2014 (using 2012 constant dollars). What's another 11 billion dollars we don't have matter, right?